Source: China Energy Storage Network News

Energy storage power stations are becoming

One of the hottest investment fields in China at present

Chen Wei, General Manager of the Engineering Consulting Department of Shanghai Jibang Investment Consulting Co., Ltd., clearly feels that the investment enthusiasm for pumped storage power stations has increased in the past two years. "In recent years, the overall enthusiasm for infrastructure investment is relatively high, but effective investment projects recognized by the market are scarce, and pumped storage power stations are one of the few options."

Local governments are the direct drivers of this boom. Since 2022, several local governments have declared the pumped storage power station project to be the "largest single investment project in history" in the region, valuing its ability to bring tax revenue and promote employment. For example, the Hunan Yanling pumped storage power station project with an investment of over 8 billion yuan is expected to achieve an annual tax revenue of over 100 million yuan, driving about 2000 people to employment.

The principle of a pumped storage power station is not complex, that is, to use the terrain difference to build two layers of reservoirs. When the power load is low, the water is pumped to the upper reservoir, and when the power load is peak, the water is discharged to the lower reservoir for power generation. The conversion of electrical energy and potential energy is used to achieve the storage of electrical energy. This is a mature technology with a history of one hundred years, and has entered China for half a century. However, its development in China has been tepid and tepid, and its importance was not highlighted until nearly two years ago.

Pumped storage power stations are only one member of the "energy storage family". "If the installed capacity of wind and solar power is increased by three times by 2030 compared to 2022, the output of power and energy storage batteries is increased by 29 times, and the output of electric vehicles is increased by 11 times, then 100% sustainability of the Earth's energy can be achieved by 2050." In the "Macro Plan" released recently by Musk, he believed that achieving a sustainable energy economy requires the allocation of 240 terawatts of energy storage.

"Some of Musk's advanced judgments are often very accurate," someone in the industry said to reporters half jokingly after hearing about this figure. As a future infrastructure, energy storage power stations are becoming one of the hottest investment areas in China.

Competing for pumped storage power station projects

In 2022, the number of approved pumping and storage power stations in China has increased from 11 in 2021 to 48, and the installed capacity has increased from 13.8 million kilowatts to 68.896 million kilowatts.

The significant jump in the number is related to the promotion of top-level planning. In September 2021, the National Energy Administration issued the "Medium and Long Term Development Plan for Pumped Storage Energy" (2021-2035) (hereinafter referred to as the "Plan"), referring to 340 key implementation projects in the medium and long term planning layout, with a total installed capacity of about 421 million kilowatts.

In April 2022, the National Development and Reform Commission requested that the approval of pumped storage projects during the "14th Five Year Plan" be accelerated in accordance with the principle of "nuclear as much as possible and open as possible", ensuring that a number of projects are approved before the end of 2022.

On December 29, 2022, the construction of the hybrid pumped storage project at the two estuaries of the Yalong River, located in Yajiang County, Ganzi Tibetan Autonomous Prefecture, Sichuan Province, was officially commenced. Upon completion, the Lianghekou Hybrid Storage Project will become the largest hybrid pumped storage project in the world. Image/Xinhua

Currently, the site of the pumped storage power station needs to be approved by the National Development and Reform Commission and included in the national plan. "However, the project approval authority is delegated to the provincial government, and once the site is approved, it can be 'for sale' and the development rights can be transferred through certain competitive procedures. Some provinces, such as Jiangxi, have issued bidding information to bid for the owners of storage projects." The aforementioned energy storage industry personage stated that power grid companies do not "take all", which brings opportunities to other investment entities.

The approval of the provincial government means that local platform companies can play their "home" advantages and more easily obtain "roads".

According to the bid winning situation of the owners of Jiangxi pumped storage projects in early 2022, among the six bid winning companies, there are both power generation enterprises such as Guodian Investment and Huaneng, as well as local state-owned enterprises such as Jiangxi Provincial Investment Group Co., Ltd. "Local state-owned enterprises and platform companies used to undertake some government public welfare projects, but now they are looking for new investment directions. Naturally, they are interested in pumped storage power station projects," Chen Wei told China News Weekly.

Previously, the main investor in pumped storage power stations was power grid companies. According to statistics, as of the beginning of 2022, the two subsidiaries of State Grid and China Southern Power Grid jointly accounted for over 90% of the installed capacity of the operating pumping and storage power stations.

Nowadays, more enterprises that have never invested in pumped storage power stations are also involved. However, it is recognized in the industry that the investment amount for pumping and storage power stations is 5000 to 6000 yuan per kilowatt, and the common investment amount for 1.2 million kilowatt pumping and storage power stations is about 7 billion yuan. This investment volume determines that the main investment entities are still central enterprises and state-owned enterprises.

Chen Wei told reporters that the new investment entities in recent years are divided into four categories: the first category is "five major and six small" power generation enterprises; The second category is new energy power generation enterprises, which overlap with the first category and have new energy allocation and storage requirements; The third category is local state-owned enterprises, including platform companies; The fourth category is infrastructure enterprises, such as power construction and energy construction, which often participated in the construction of water conservancy projects in the past, as well as CSCEC and CCCC. "Although the investment logic is different, these four types of enterprises are all competing for pumped storage power station projects."

"The number of suitable sites is limited, and given the sites that have been launched and stored, there is little room for future incremental growth," Chen Wei said. The key to selecting the location of pumping and storage power stations is to consider the natural endowment of mountains and water resources. The existing pumping and storage power stations are mainly distributed in load centers such as East China and South China. Due to resource advantages, Guangdong, Zhejiang, Anhui, and Jiangsu currently rank among the top four provinces in terms of installed capacity of pumped storage power stations.

Chen Wei believes that most of the 340 projects in the plan are large pumped storage power stations, and there is still room for growth in the future of hybrid, hundreds of thousands of kilowatt grade small and medium-sized pumped storage power stations. "Currently, most of the pumping and storage power stations approved and operating in this round have an installed capacity of more than 1.2 million kilowatts, and there are really few sites available for this level of pumping and storage power stations."

The limited site and high investment threshold make pumped storage investment seem hot, but industry insiders generally believe that there is no need to worry about excessive investment in the short term, especially considering that the installed capacity of new energy is still rising rapidly.

Insufficient quantity of "Super Power Bank"

Pumped storage is currently the most mature technology for large capacity energy storage, and large pumped storage power stations are often described as "super charging banks.".

For example, the Fengning Power Station in Hebei has created the world's largest "super charging bank", which can store nearly 40 million kilowatt hours of new energy at one time and absorb 8.7 billion kilowatt hours of new energy throughout the year. It plays a large capacity energy storage role in supporting the safe and stable operation of the North China Grid and enhancing the regulatory capacity of the power system.

The absorption of new energy is the most critical mission for the birth of energy storage. Electric power has the characteristic of real-time balance between supply and demand. However, as the installed capacity of renewable energy sources such as wind and light increases, the randomness, volatility, and intermittency of the power supply side increase, and the power system needs more flexibility to adjust the power supply.

According to the "14th Five Year Plan" for Modern Energy System Planning, by 2025, the proportion of flexible regulated power sources in the installed capacity of the power system will reach about 24%. However, at present, China's flexible adjustment resources are very scarce. By the end of the "13th Five Year Plan" period, even with the addition of the installed capacity of thermal power flexible transformation, the total proportion is about 18.5%, while the proportion of flexible adjustment resources in Western countries exceeds 30%.

There are many ways to increase flexible adjustment resources. "For example, 'wind-solar complementarity' is a combination of wind power and photovoltaic power to achieve stable output on the power supply side, that is, sufficient sunlight during the day, and photovoltaic output is dominant. At night, the wind force is usually relatively strong, and wind power output is dominant. However, the actual situation is that in the evening, there is often no light and small wind, but it is at the peak of load. Another example is to achieve wind fire and light fire bundling through flexible transformation of thermal power units, but only when the installed capacity is' more thermal power, less wind power '. Technically "It is possible to achieve this. Once the installed capacity of renewable energy accounts for an absolute majority, thermal power is difficult to support in terms of capacity." Chen Haisheng, chairman of the Zhongguancun Energy Storage Industry Technology Alliance, told China Newsweek that only by adding flexible resources such as energy storage in the power system can the problem be fundamentally solved.

However, the current installed capacity of energy storage is significantly insufficient. Chen Haisheng said that according to the prediction of relevant departments, the installed capacity of renewable energy will reach about 5 billion kilowatts in 2060, and the average annual installed capacity for the next 40 years will be between 100 million and 150 million kilowatts. In a high proportion of renewable energy scenarios, it is necessary to account for 10% to 15% of the total installed capacity of energy storage to ensure stable power supply and security of the power system. However, the current proportion in China is about 2%, and "there is still significant room for growth in the future.".

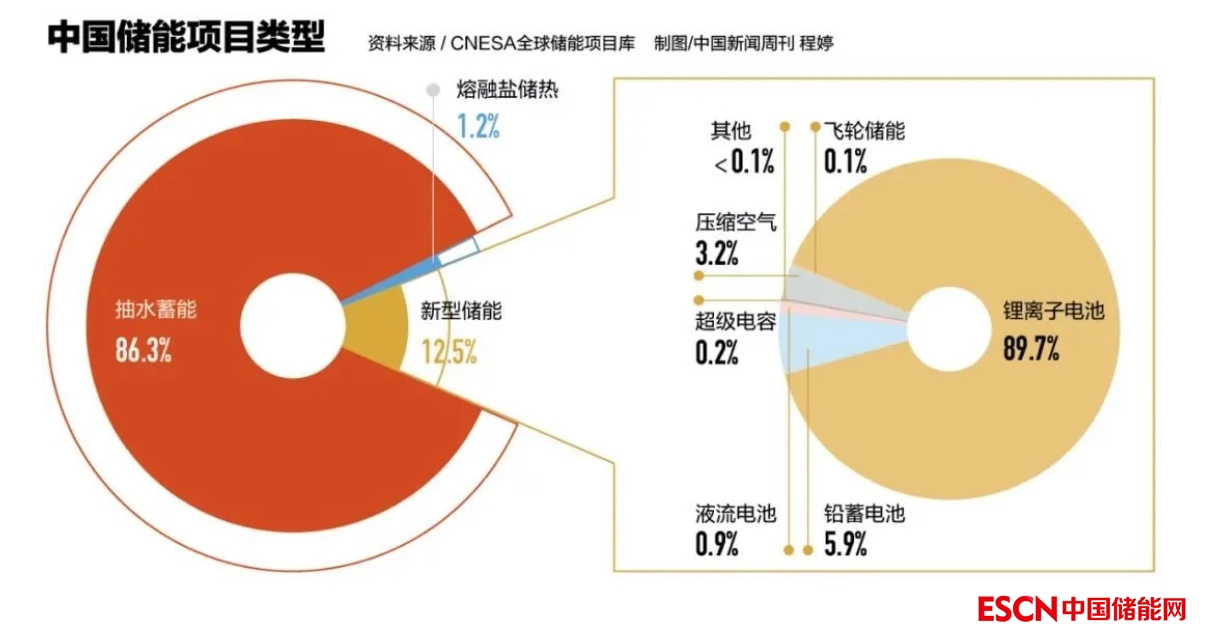

By the end of 2021, among the energy storage projects that have been put into operation in China, pumping and storage power stations account for 86.3%, making them the absolute mainstay. However, before 2021, the development of pumped storage power stations in China was once "stalled".

In documents such as the "12th Five Year Plan" for energy, the goal of 30 million kilowatts of pumped storage installed capacity by the end of 2015 and 70 million kilowatts by the end of 2020 was set, but by the end of 2020, only 31.49 million kilowatts of installed capacity had been completed, far behind the plan.

"As early as 2015, the National Energy Administration encouraged more entities to participate in investment in pumped storage power stations. In the era of grid enterprises as investment entities in pumped storage power stations, they were more positioned in grid side infrastructure, with unclear investment mechanisms, and therefore did not have investment attributes." Chen Wei told reporters.

In May 2021, the National Development and Reform Commission issued the "Opinions on Further Improving the Pricing Mechanism for Pumped Storage Energy" (hereinafter referred to as the "633 Document"), clarifying the "two part system" electricity pricing policy, forming electricity pricing in a competitive manner, and incorporating capacity pricing into the recovery of power grid transmission and distribution pricing, to determine a capital internal rate of return of 6.5% for capacity pricing.

This means that the pumped storage power station can recover its operating costs through the electricity price difference between charging and discharging. At the same time, the capacity price is a fixed income, independent of the amount of electricity generated.

"The No. 633 document establishes a business model for pumped storage power stations, which also makes pumped storage power station projects a 'hot potato'." Chen Wei told reporters that the current financing difficulty of pumped storage projects is very low, because it means a stable business model and government endorsement, and banks have less risk control concerns.

Many people in the energy storage industry believe that the electricity price mechanism for pumped storage can be quickly straightened out, in large part because power grid companies are also important investors, and all parties agree. "The capacity electricity price is included in the transmission and distribution electricity price, which is paid by the power grid company in advance, but ultimately transmitted downward, and the cost is shared by the entire society, because pumped storage power stations are regarded as the infrastructure of the power system and have a public welfare attribute."

The approval and commencement of pumping and storage power stations with rationalized business models are entering the fast lane, but it is still difficult to meet demand.

New energy storage competing for excellence

The long construction period is often regarded as the "short board" of pumped storage power stations.

Gu Yu, Vice President of Weijing Energy Storage, told China News Weekly that the construction cycle of the pumped storage power station is relatively long, at least in 6 to 7 years. In addition, pumping and storage power stations were at a low investment point before, and a batch of projects that were centrally approved and started in 2022 will not enter the peak of production until 2030, which is clearly difficult to match the growth in installed capacity of renewable energy in recent years. "When communicating with some local governments, the other party also mentioned that 'it is difficult to quench thirst from afar', and it is impossible to wait until all the pumping and storage power stations are put into operation before installing the wind turbine."

This also brings opportunities for new energy storage. The so-called new energy storage refers to other energy storage technology routes other than pumped storage, in which electrochemical energy storage represented by lithium ion batteries is mainly used. By the end of 2022, among the new energy storage installations nationwide, lithium ion batteries accounted for 94.5% of energy storage, compressed air accounted for 2.0%, liquid flow batteries accounted for 1.6%, lead acid (carbon) batteries accounted for 1.7%, and other technical routes accounted for 0.2%.

"It is expected that before the peak of operation of pumped storage power station projects under construction is ushered in from 2028 to 2030, the new type of energy storage is expected to experience rapid growth due to its strong site selection flexibility and short installation and commissioning cycles, which are mostly 2-3 months, and some large projects are expected to last for about half a year." Liu Yong, Secretary General of the Energy Storage Application Branch of the China Chemical and Physical Power Industry Association, told China News Weekly.

"Apart from the factor that 'water far away is difficult to quench thirst near', relying solely on the mature technical route of pumped storage is also difficult to meet the entire demand for energy storage in the future power system." This is an industry consensus. According to the statistics of the Zhongguancun Energy Storage Industry Technology Alliance, there is a demand for energy storage in power generation, transmission, distribution, and utilization, which can be subdivided into 18 types. Different energy storage technology routes correspond to different application scenarios.

"Taking lithium ion batteries as an example, they have high energy density and efficiency, and are suitable for distributed energy systems and user side energy storage, with a relatively small scale and a capacity of one or two hours. On the other hand, pumped storage belongs to long-term, large capacity energy storage, with a capacity of basically more than 4 hours, and is suitable for grid side 'peak shaving and valley filling'. The two can form complementary advantages." The head of a new type of energy storage enterprise told China News Weekly, There is no one technological route that can "unify the country.".

He believes that the national strategy for pumped storage power stations is to "build as much as possible", so the installed capacity of pumped storage power stations will still increase, but the market share will gradually decline. By the end of 2021, the installed capacity of domestic pumped storage power stations had accounted for less than 90%. "Seven or eight years ago, this proportion reached around 99%, when energy storage power stations were equivalent to pumped storage power stations."

At present, local governments are no less enthusiastic about the implementation and industrial layout of new energy storage projects than pumped storage, and are "working hard and quickly". A person in charge of a new type of energy storage enterprise sighed to the reporter that investment promotion teams from various regions are queuing up to visit the enterprise, receiving three or four groups of investment promotion personnel every week.

In July 2021, the National Development and Reform Commission and the Energy Administration issued the "Guiding Opinions on Accelerating the Development of New Energy Storage" (hereinafter referred to as the "Guiding Opinions"). It is planned that by 2025, the installed capacity of new energy storage will reach over 30 gigawatts, an increase of more than 8 times compared to 2020. Liu Yong told reporters that last year, the newly installed capacity of new energy storage reached 5.6 gigawatts, compared to only 2 gigawatts the previous year. With the goal of completing a new energy storage capacity of 30 gigawatts by 2025, it is now close to completing 10 gigawatts, and there is not much pressure to achieve the goal.

According to the statistics of the Zhongguancun Energy Storage Industry Technology Alliance, as of December 2022, nearly 30 provinces across the country have issued new energy storage plans or new energy configuration and storage documents for the "14th Five Year Plan", with a total development goal of over 60 gigawatts, twice the target of reaching 30 gigawatts by 2025 proposed in the guidance.

"Unlike the approval of the National Development and Reform Commission for the location of pumped storage power stations, new energy storage plans are made by provinces based on their own actual conditions, and even some prefecture-level cities have launched plans, such as Tai'an City, Shandong Province, which proposed to build a 'energy storage city' of tens of millions of kilowatts. If the target of 60 gigawatts can be achieved by 2025, local governments need to consider how to improve utilization efficiency and avoid 'building without using', and must be combined with local power grid planning "Think about the function and value of new energy storage in terms of power supply structure." Liu Yong said.

Chen Haisheng introduced to reporters that the 60 GW energy storage plan is a new installed capacity for energy storage proposed by provinces after considering resources such as thermal power flexibility transformation and demand side response, reflecting the significant demand for energy storage in each province. On the other hand, all localities should avoid "crowding in" when their business models are not mature, and should effectively choose appropriate technological route development methods to ensure the implementation of energy storage industry planning.

Currently, various provinces have launched demonstration projects, on the one hand exploring technical issues such as system integration of some new energy storage technologies at the level of 100 megawatts and gigawatts, and on the other hand exploring business models.

The market determines the future technology route

Gu Yu believes that the reason why lithium batteries became a new force in the new energy storage market at the beginning is because lithium products are more mature.

However, the situation where lithium batteries dominate 90% of the new energy storage market may be facing an impact. "In some Western countries, long-term energy storage has been a key development direction. During the COP 26 climate negotiations, the Long Term Energy Storage Council was established, and none of the electrochemical energy storage companies chose the lithium ion battery technology path. The important reason is the high cost of lithium electricity." Chen Jingning, General Manager of Shanghai Haipu Sodium Energy Technology Co., Ltd., told China News Weekly, The demand for batteries in the energy storage market is more than ten times that of the power battery market, and the huge demand makes energy storage extremely sensitive to costs.

With the rising price of lithium carbonate, the main raw material for lithium batteries, this contradiction has become increasingly acute.

The application of lithium batteries to new energy vehicles broke out in the second half of 2014. Before 2020, the price of lithium carbonate stabilized between 30000 and 50000 yuan/ton, but it has stabilized at over 400000 yuan/ton in the past two years. The selling price of lithium ion energy storage batteries is about 0.9 yuan/watt hour, lower than the 1.1 to 1.2 yuan/watt hour of new energy vehicles, and more pressure is felt from the rising cost of raw materials.

"Currently, there are many technical routes, but the production capacity is far from enough." Gu Yu told reporters that the most lacking this year is not orders but production capacity. Whether domestic or foreign, there are many people consulting orders, and they have projects in hand, but are looking for products. The company is stepping up the layout of liquid battery factories in Yancheng, Zhuhai, and other places.

The market is also enthusiastic about investing in new types of energy storage other than lithium batteries. "There are already central and state-owned enterprises willing to invest in compressed air energy storage power stations, which have gradually recognized this technological direction compared to previous years. Compressed air energy storage power stations are heavy asset projects, and their high capital costs have made them the main investment force. However, there are also some private enterprises that hope to invest in the project construction period for a short period of time, and the project will be transferred to central and state-owned enterprises when it reaches a certain stage." A person in charge of a compressed air energy storage enterprise told China News Weekly.

However, he still envies that the pumped storage power station has established a sound pricing mechanism. "To be realistic, it is very difficult to finance debt financing for new energy storage projects, including compressed air energy storage, because its electricity price policy is not yet clear, and it is difficult to determine whether it can form a business model with stable returns."

In June 2022, the National Development and Reform Commission and the National Energy Administration issued the Notice on Further Promoting the Participation of New Energy Storage in the Electricity Market and Dispatching Application, further clarifying the positioning of the new energy storage market and promoting the participation of independent energy storage in the market.

Various regions are also exploring possible business models in combination with demonstration projects. Shandong has launched two batches of demonstration projects, and the benefits of energy storage power stations come from several aspects: First, participating in spot trading in the electricity market. In December 2021, Shandong launched spot trading in the electricity market. Like stocks, electricity prices follow the market, and energy storage power stations can "buy low and sell high.". Second, Shandong is both a province with large production capacity and a province with large energy consumption, but there is a lack of regulatory means. The energy storage power stations in two demonstration projects can receive small subsidies when providing peak shaving services. The third is the rental income of energy storage indicators. Shandong forces new energy power stations to build 20% of the installed capacity of energy storage, but it is not necessarily self built by new energy power stations, but can share the energy storage, thereby obtaining the indicator rental income.

Liu Yong believes that "at present, the installation speed of energy storage power stations is difficult to match the new energy installation process. The important reason is that the business model of energy storage power stations is still being explored, and a cost mitigation mechanism has not been fully established."

As the 633 document changes the fate of pumped storage power stations, many practitioners are still waiting in the energy storage market, which is highly influenced by policies. "In the competition for various new energy storage technology routes, the regulatory attitude is clear, leaving it to the market to choose. Safety, environmental protection, and cost control are the 'impossible triangle' of the energy system, and the role of energy storage is to make it a 'possible triangle'. As long as an energy storage technology can meet these three conditions, the market must have a position to accept." Gu Yu believes that the current energy storage market in China is "competing for competition among hundreds of competitors.", Instead of "killing each other".